|

Capitalism: global restructuring, sovereign debt, benign bloc politics and safety nets ('HTML Version ''EPUB Version: ''MOBI Version: ''PDF Version: ') Bill Geddes

We've lost control. Unregulated internationalized capitalism is in the driving seat, and it is demanding that countries, communities and individuals subordinate themselves to its needs and interests1 . As countries find themselves with unmanageable sovereign debt2 , they are being subjected to 'structural adjustment' to make them more accountable - and vulnerable - to an internationalized capitalism which has gained the whip hand. It now demands that we accept our lot; that we reduce our lives and our vision to its horizons; that we accept that we are nothing more than a malleable, expendable 'workforce' for its activities and a 'consumer base' for its products. As this happens, you and I are similarly being 'adjusted' to the requirements of an unregulated capitalist world 3 . As Peter Coy and his co-writers explained: Peter Cappelli, director of the Center for Human Resources at the University of Pennsylvania's Wharton School, says the brutal recession has prompted more companies to create just-in-time labor forces that can be turned on and off like a spigot. "Employers are trying to get rid of all fixed costs," Cappelli

says. "First they did it with employment benefits. Now they're doing it with the

jobs themselves. Everything is variable." That means companies hold all the

power, and "all the risks are pushed on to employees." It's time to take back control of our communities and our individual lives. It's time to make capitalism the servant and not the master of countries, communities and individuals4 . Let's indulge ourselves and pretend that the future could be kinder, gentler than the present; that human beings might cooperate for the good of all rather than indulging their darker urges. What if Europe's leaders decided to protect their populations from the ravages of unregulated capitalism, making capitalism the servant rather than master of the Eurozone? How wonderful it would be if, instead of predictably travelling down the path of deregulation, erosion of working/ living conditions and reduction of welfare provisions to the lowest common denominators of member states 5 , Eurozone leaders decided to reverse the process. When I listen to Angela Merkel and Nicolas Sarkozy I sometimes believe I hear a tentative, nostalgic inclination toward this (perhaps I'm delusional, or perhaps it's double-speak - after all, Germany, the 'economic power-house' of Europe is one of the countries setting Europe's lowest common denominators. Amongst other things, it does not have a universal minimum wage 6 )! For many years I have admired the French determination to retain minimum welfare and labor standards in the face of international pressures for deregulation. Of course, there has been an implied but fundamental contradiction involved in this determination. On the one hand, France has wanted to become a member of the club of internationalized capitalist nations; on the other, it wants to retain those minimum labor, living and welfare conditions, hard-won during earlier times of regulation and protection. As Sarkozy rightly argues, you can't have both!7 But, perhaps a united Europe could retain minimum standards. France's Sarkozy reforms of the past few years could be rolled back, re-establishing those minimum labor and welfare protections to which France was previously committed. Those standards could become the standards of a united Europe. A Europe dedicated to guaranteeing the quality of life of all its inhabitants. We could have a set of standard minimum conditions for all of Europe's member states! What? This would make the Eurozone (including Germany) internationally 'uncompetitive'? Of course it would - so long as the Eurozone remains an unprotected servant of unregulated, internationalized capitalism! But, remember, we are aiming to tame capitalism, making it servant not master. Yes, that would require a 'protected' Europe - Europe with a protected working, living and welfare environment, with a social welfare safety net! Yes, that would still require some structural readjustment in Greece, Spain, Italy and other European states which have even more civilized working and welfare conditions than France used to have (unless, of course, those higher standards were used as the base for reform!), but at least we'd now have Eurozone-wide sets of minimum working and welfare conditions to safeguard populations from free-market exploitation - we would not have an expanding population of 'working poor' and destitute retirees8 . Yes, that would require the introduction of welfare measures in those states where, until now, the least advantaged have not been protected from the ravages of unregulated capitalism. Until now, those states have, by default, slowly but inevitably eroded the living standards of Europe. It would, at last, be a united Europe with a soul!! Yes, it would require increases in various business-oriented revenue generating taxes and charges to deal with the current sovereign debt problems of its member states; more than a little 'protectionism'; the introduction of tariffs on imports; the stimulation of Eurozone enterprise; and centralized fiscal and financial management. And, yes, that does imply 'bloc politics' for the Eurozone - isn't that what the current EU organization is about? Yes, that would require individual states to accept minimum Euro-wide sets of regulations in the interests of the well-being of their populations. Without such regulation, individual states would find themselves subjected to the demands of international capital, played off against each other in a 'race to the bottom'. Remember, we're taming unregulated capitalism, not trying to accommodate it! Second, the USA - and this could be much

simpler! In the USA we find the heart of the deregulation dogmas of the past forty years. Here is the triumph of neoliberalism, the final defeat of 'The New Deal' 9 . Not even the wars of the past decade have managed to rescue the nation from the consequences of that unregulated, internationalized capitalism, unleashed on us all by the devotees of those dogmas. In previous decades US administrations have used such conflicts as a means of triggering an implicit Keynesianism. It has stimulated internal, protected economic activity through 'defense' expenditures in United States' communities. Congressional competition for home state funding has ensured a wide distribution of such stimulus funds. And, all the while, it has claimed that 'national security' required these expenditures to be contained within the borders of the nation. But, over the past forty years it has allowed its internal protections to be eroded, resulting in a massive hemorrhaging of funds to the rest of the world. Any attempt at similar internal economic stimulus would now simply compound its problems. In urban, sub-urban and rural areas, we find communities abandoned to their fate, stripped of assets and wellbeing, slowly, but inevitably decaying, thrown on the scrapheap of unregulated internationalized capitalism 10 . And this could so easily be reversed - all it requires is a reversion to the double-standards of previous decades - talk free market, but practice protected Keynesian economic activity 11 . Of course, since US politicians and populations now believe in unregulated internationalized capitalism, it would be almost impossible to prevent the external hemorrhaging of internal stimulus funding through purchase of imported goods and services. So, if the US is to kick-start its economy and not simply compound its deficit problems there will need to be legislation in place to limit the outflow of US currency. Yes, that is going to mean re-regulation! What the heck! Let's call a spade a spade - it's going to mean 'protection'. Asian nations have both a problem and an opportunity. First, their growth has largely been based on supplying low cost products and services to Western nations. Even where they have managed to move to higher-end products and services, largely, their competitive edge has been the provision of high quality items at a lower cost than can often be achieved in Western countries 12 . In order to retain their competitive advantage, Asian nations are largely locked in to minimal working/living and welfare conditions for the bulk of their populations. If they are significantly to improve those conditions, they will need to break free from dependence on exports to Western destinations 13 . Of course, if Western nations did re-regulate, this competitive edge would largely disappear - dissipated by tariff and other adjustments at ports of entry. The current economic strength of Asian countries lies in their development of strongly export-oriented economic growth, coupled with a lower internal per capita demand for goods and services. This results in strong export/import surpluses, a 'savings' mentality, and the internalization of sovereign debt. As in Japan, the sovereign debt, while huge 14 , is largely owed to Japanese rather than external funders 15 . In the last month, Japan, South Korea and China16 have formalized a move to direct trading of their currencies, effectively creating a 'common market' which excludes both US and Eurozone currencies 17 . I have, for the past several decades, been intrigued by Japan's apparent ability to ignore its deficits. It's as though the numbers are not 'real', just characters on a page which can be turned without concern. I suspect that this is because, deep down, Japan is not a capitalist country! It is just playing a 'capitalist game', akin to the board game 'monopoly'. Its books don't have to balance, its corporations don't have to abide by the 'rules of capitalism'; they only have to appear to do so for the sake of their 'international image'. I suspect that China and South Korea share this same detachment. And, I suspect that if one examined other East and South East Asian countries and communities one would find a similar sense of the unreality of the game. This gives them a wonderful advantage! They don't have to wake in the middle of the night in a cold sweat, panicking at the size of their deficits, wondering how one earth they are going to 'make ends meet'. Even their 'surpluses' are in some measure 'unreal', handy counters in an international game in which those with apparent surpluses hold the whip hand. How wonderful it would be if, while they are still relatively insulated from the traumas of Western-style internationalized capitalism, they could reinvent capitalism to suit their own internal purposes, making it servant to the prosperity of their peoples, while retaining the advantages of not taking the game seriously. Yes, this would require 'bloc' politics, with Asian nations forming their own 'common market', generating their own internalized economic dynamic and raison d'être. And, yes, this would require bloc-wide regulatory structures and conditions to ensure the well-being of their peoples. In my Dreaming I imagine Asian countries finally reinventing capitalism, tailoring it to the needs and interests of their various communities; making it servant to, not master of, their futures. And, since it is only a dream, I see Western nations finally coming to their senses, learning from Asia and taming and shaping capitalism to ensure benign and supportive working/living/welfare conditions for all their inhabitants. But, I guess the age of utopian dreams and schemes is in the past 18 . We are left with the stark reality of a world where unregulated capitalism reduces humanity to a 'resource'; where countries, communities and individuals are 'restructured' to the demands and requirements of an asocial capitalism which need accept no responsibility for their well-being and their futures. It looks as though, if our political leaders have their way, we will have to resign ourselves to being, forever, merely a 'workforce' and 'consumer base' for unregulated, internationalized capitalism's activities and products!

Endnotes 1 Ulrika Lomas (Tax News, 14 Dec. 2011) described Sarkozy's determination to reinvent France and the rest of the Eurozone to meet 'rating agency' demands (before the downgrading!): Providing his assurances that the commitments undertaken by France will be respected, the French President explained that the government has already taken, or is in the process of taking, the necessary measures to convince investors. According to President Sarkozy if the government had not embarked upon pension reform in France in 2010, accelerated recently with the framework of the country's second austerity package, it would only be delaying the inevitable. Otherwise, there is no key measure or 'miracle', Sarkozy remarked, noting that what counts ultimately, as much as measures aimed at reducing spending, are initiatives intended to increase growth, for example the development of the research tax credit and the abolition of local business tax in France... According to Sarkozy, the agreement responded to the crisis and to the concerns of rating agencies... The BBC reported France's subsequent credit rating downgrade (14 January 12 13:04 GMT): French PM Francois Fillon has defended his government's economic policies following the decision by ratings agency Standard and Poor's to downgrade the credit rating of France. He said the government would push ahead with reforms and debt reduction. Standard and Poor's said Europe's austerity and budget discipline alone were not sufficient to fight the debt crisis and may become self-defeating. The downgrade stripping France of its top AAA rating was announced on Friday. The government is on a communications campaign to tell the

French there is no need to panic and that the policies of reform and debt

reduction will continue as planned, says the BBC's Hugh Schofield in Paris.

Reassuringly, as David Beer of Standard and Poor explained in a CNBC interview, rating agencies do not have a 'hit list'. As school-masters of economies, they discipline anyone who does not perform as they believe they should: After Standard and Poor's historic downgrade of the U.S.'s credit rating to AA-plus from triple-A, fears are growing that other countries may be next, most notably France, which is facing big costs from a bailout of troubled Euro zone countries. But the global head of sovereign ratings at S&P says the agency does not have a target list and will downgrade ratings as and when it sees deteriorating economic performance or debt burdens. "We don't have a hit list, we've obviously taken a number of

rating actions in the Euro zone going back a number of years, that's still an

unfolding story which we're watching very closely," David Beers told CNBC on

Monday. 2 See Global economic forces, Western realities; Comparison of holders of sovereign debt for more on this. For a detailed comparison of the external debt data of countries see World Bank Quarterly External Debt Statistics. 3 Peter Coy, Michelle Conlin and Moira Herbst (Bloomberg Businessweek January 7, 2010 ) spelt out the consequences for individuals: You know American workers are in bad shape when a low-paying, no-benefits job is considered a sweet deal. Their situation isn't likely to improve soon; some economists predict it will be years, not months, before employees regain any semblance of bargaining power. That's because this recession's unusual ferocity has accelerated trends-including offshoring, automation, the decline of labor unions' influence, new management techniques, and regulatory changes-that already had been eroding workers' economic standing. The forecast for the next five to 10 years: more of the same, with paltry pay gains, worsening working conditions, and little job security. Right on up to the C-suite, more jobs will be freelance and temporary, and even seemingly permanent positions will be at greater risk. "When I hear people talk about temp vs. permanent jobs, I

laugh," says Barry Asin, chief analyst at the Los Altos (Calif.) labor-analysis

firm Staffing Industry Analysts. "The idea that any job is permanent has been

well proven not to be true." As Kelly Services (KELYA) CEO Carl Camden puts it:

"We're all temps now." David Wessel (Wall Street Journal July 27, 2011 ) put it succinctly: Over the past 10 years:

What's wrong with the American job engine? As United Technologies Corp. Chief Financial Officer Greg Hayes put it recently: "Sales have come back, but people have not.'' That's largely because the economy is growing much too slowly to absorb the available work force, and industries that usually hire early in a recovery-construction and small businesses-were crippled by the credit bust. Then there's the confidence factor. If employers were sure they could sell more, they would hire more. If they were less uncertain about everything from the durability of the recovery to the details of regulation, they would be more inclined to step up their hiring. Something else is going on, too, a phenomenon that predates the recession and has persisted through it: Changes in the way the job market works and how employers view labor. Executives call it "structural cost reduction" or "flexibility."

Northwestern University economist Robert Gordon calls it the rise of "the

disposable worker," shorthand for a push by businesses to cut labor costs

wherever they can, to an almost unprecedented degree. See Just-In-Time and Total-Quality-Control: Let's be flexible! for more on this. 4 In an unregulated internationalized capitalist world, the weak are vulnerable. If individual countries attempt to tame capitalism they will fail. The only way in which capitalism might possibly be tailored to communities, rather than communities to capitalism, is through banding together. It's time for 'bloc politics', for groups of nations to band together, forming large enough units to become internally economically viable. Of course, the problem of 'unattached' regions, those which seem, inevitably, to fall outside of the bounds of major blocs, is a problem which has always existed, and will continue to exist into the future. In the past people living in such regions have been prime candidates for exploitation, unable to protect themselves from the predations of organized and dominant power blocs of the world. Perhaps a fortified United Nations could provide a regulatory umbrella under which they might shelter. 5 and, over time, to the lowest common denominators of the world. Michael Birnbaum (2012), in a Washington Post article, described the consequences of this process in the Eurozone for Greece: ...many Greeks question whether the terms of the bailout will do much to help their economy in the coming years, and the 'troika' of the International Monetary Fund, European Union and European Central Bank acknowledged that the recession would worsen in the short run, even as unemployment has already spiked to 21 percent - 49 percent for those younger than 25 - and the economy contracted by 7 percent in the third quarter of 2011. Europe has demanded that the public sector shrink by 150,000 people, that the minimum wage be lowered by 22 percent, that pensions be cut and that Greece do more to sell off its publicly owned companies, among other measures that filled a 50-page booklet. When the Greek parliament started implementing them last week,

43 of the deputies in the ruling coalition rebelled, and rioters in Athens set dozens of buildings on fire. 6 See Information on Minimum Wage Rates for more on this. An article in The Economist (Nov. 5th 2011) explained: Germany is one of the few European countries to lack a statutory minimum wage. Unions and employers negotiate wages sector by sector. In ten sectors agreed minimums apply to all. But jobs are growing in fragmented services not in manufacturing. Just over half of workers in western Germany are now covered by central agreements; in the east it is only a third. In 2007, 3.7m workers earned under €7 ($9) an hour and 1.2m under €5. Angela Merkel's recently expressed determination not to carry the debt load of other EU countries should be understood in this context. Germany has effectively weakened social welfare guarantees for its own population, accepting an increasing number of 'working poor' as the social cost for its economic expansion. If it now accepts responsibility for using its consequent economic muscle to underwrite countries which have retained social welfare guarantees, it is effectively sacrificing the wellbeing of up to half of its own population for the ongoing wellbeing of other EU populations. Some reader comments on the minimum wage appended to the above article seem sadly in tune with similar comments made by middle ranking Western Europeans in the 18th and 19th centuries. See The Virtuous Capitalist, The Poor and the Wasteland for more on this. 7 The pressures for change which France faces in an unregulated internationalized capitalist world cannot be avoided by changing the leadership, as the new French President Francois Hollande has found. A Bloomberg report (July 12, 2012) explains the problem: On July 12, Peugeot announced it will close a factory in the Paris suburbs and cut thousands of jobs at other facilities. Including reductions announced last year, it's set to shed some 14,000 workers, mainly in France. Prime Minister Jean-Marc Ayrault called the announcement 'a true shock.' Peugeot had little choice. It will post a €700 million ($860 million) first-half operating loss and is burning through €200 million in cash every month. The carmaker's factories are operating at just 76 percent capacity, as first-half deliveries slid 13 percent. To raise cash and cut debt, it's selling off assets, including its Paris headquarters. 'Peugeot is pretty close to bankrupt,' says Nicolas Meilhan, a Paris-based consultant at Frost & Sullivan who previously worked for the car company. Other European automakers have suffered sales declines during the region's debt crisis, but Peugeot's problems go far deeper than its rivals'. Some 40 percent of its production capacity is in France, where high payroll taxes and rigid labor rules clobber its competitiveness, Meilhan says. French unit labor costs, now the second-highest in Europe after Belgium, have increased about 20 percent in 2000 in relation to Germany, benefiting competitors such as Volkswagen (VOW3). French automaker Renault (RNO) is in much better shape than Peugeot, as it has moved 80 percent of production abroad, mainly to low-cost locales. The news from Peugeot only adds to an increasingly dire economic

outlook in France. Unemployment is at 10.2 percent, and the government recently

downgraded its 2012 growth forecast to just 0.3 percent. Two other big

employers, Air France (AF) and pharmaceutical group Sanofi (SNY), have announced

major job cuts since Hollande took office in May. 8 See Community costs are Production costs for more on this 9 See The triumph of neoliberalism for more on this. 10 Rick Hampson (USA Today 3/2/2010) described the scene (still being played out in 2012) across the United States: Whether it's textiles in the Carolinas, paper in New England or steel in the Midwest, most industrial cities and mill towns "are on pins and needles," says Donald Schunk, an economist at Coastal Carolina University. "Day to day, week to week, any manufacturing facility seems vulnerable. People don't know if they'll be there." That's true in:

Anxiety over possible layoffs or closings can disturb workers as much as the real thing, experts say. Harvard psychologist Daniel Gilbert says it's uncertainty that really bothers people: They feel worse when they think something bad might happen than they do when they know it will happen.... In the America where things are made, the recession has been a depression. According to a new Northeastern University study, one in every six blue-collar industrial jobs have disappeared since 2007, matching the drop in overall employment in the Great Depression. Last year, about 1.3 million factory jobs vanished, including Shumaker's. For the first time, the government announced in January, most union members are government employees, not private-sector workers. One-horse towns such as Ravenswood risk losing their reason for being, says Juravich, who teaches about labor at the University of Massachusetts. Without a hospital or university campus or county seat, "they're one plant shutdown from oblivion." Sometimes oblivion is a ghost town with tumbleweed blowing down Main Street and the doors of the Last Chance Saloon swinging in the desert wind. But most 21st-century ghost towns will not be deserted. People, many unemployed or underemployed, will fill the bars, stoops, corners, clinics, jails and social welfare offices. An industrial town makes products that bring wealth into a community; a post-industrial ghost town has a zero-sum economy - people in marginal jobs, "serving and paying each other," Bronfenbrenner says. At best, the new industrial ghost towns become places for

low-rent homes for long-distance commuters. At worst, they slowly empty

out. See Ilyce Glink, CBS News January 12, 2012, Foreclosures hit lowest level since 2007, for discussion of the foreclosure difficulties still facing homeowners across the US: Foreclosure filings dropped in 2011 to their lowest level since 2007, according to a new report released today from RealtyTrac. Unfortunately, the lower number of foreclosures doesn't mean fewer people are going to lose their homes. Just the opposite. According to RealtyTrac's Year-End 2011 U.S. Foreclosure Market Report, the number of foreclosures declined because lenders stopped processing foreclosures and created a huge backlog in the foreclosure pipeline. According to RealtyTrac's report, some 2,698,967 foreclosure filings -- which include default notices, scheduled auctions and bank repossessions -- were reported on 1,887,777 U.S. properties in 2011, a decrease of 34 percent from 2010. About 1.45 percent of all U.S. housing units (about 1 in 69) received a foreclosure filing last year. That's the good news, but the time it took to process those foreclosures increased 24 percent over the same time period. This increase in foreclosure processing time has largely been caused by the robosigning controversy, which triggered lenders to perform a massive review of foreclosure procedures. This review of the foreclosure process caused lenders to hold off on beginning many new filings, which is a big contributor to the lower number of foreclosures in 2012. According to Brandon Moore, CEO of RealtyTrac, "Foreclosures were in full delay mode in 2011, resulting in a dramatic drop in foreclosure activity for the year."... The time it takes to process a foreclosure will probably remain high through 2012, and it is likely foreclosure filings will increase in the coming year. "The lack of clarity regarding many of the documentation and legal issues plaguing the foreclosure industry means that we are continuing to see a highly dysfunctional foreclosure process that is inefficiently dealing with delinquent mortgages -- particularly in states with a judicial foreclosure process," Moore says.... For a full review of the study and a map of foreclosure activity

nationwide, see RealtyTrac's full Year-End 2011 U.S. Foreclosure Market Report. 11 One can only hope that, should the US revert to its former practices, US politicians will finally find a less belligerent justification for internal economic stimulus than 'external threat'. 12 Unless, like Germany, they have managed to avoid or substantially reduce the various welfare imposts of the pre-globalization era. 13 See The emergence of welfarism: Social costs are Production Costs for a brief outline and explanation of the emergence of coherent sets of minimum working/living and welfare conditions for Western populations. 14 Edward Chancellor (Financial Times, Nov. 1, 2009) explained: Japan's national debt is fast approaching 200 per cent of GDP. The debt mountain is the result of prolonged economic weakness and successive fiscal deficits since the bubble economy collapsed in 1990. These problems are compounded by the fact that Japan's population is now shrinking. The economy's trend growth rate has fallen and tax receipts are shrinking, while welfare payments for pensioners are rising. Japan's debt trap, it seems, is structural rather than cyclical.... Tokyo has shown little serious intent on getting its public finances under control. The newly-installed DPJ government didn't even mention the deficit in its election manifesto. This passivity brings to mind David Hume's comment that 'when a government has mortgaged all its revenues... it necessarily sinks into a state of languor, inactivity and impotence.'... Other countries with oversized national debts, such as Sweden after the Scandinavian banking crisis of the early 1990s, were able to generate growth by devaluing their currencies and boosting exports. The yen, however, has strengthened. Interest rates in Japan have been low for so long that all the gains from low cost financing have already been spent. While the supply of Japanese government bonds looks set to increase, the outlook for demand is not encouraging. As the population ages, Japanese pension funds are more likely to be selling bonds than buying them. The household savings rate is plunging towards zero. As Reinhart and Rogoff observe, sovereign debt crises have often

been anticipated by governments being forced to borrow at ever shorter

maturities. For the moment, Japan's savers seem content to lend to their

government at very low rates. One day they might start demanding more for the

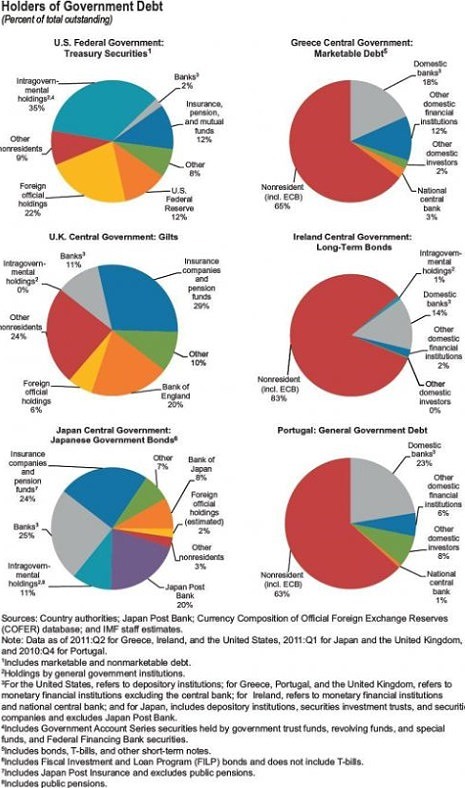

risks they are running. 15 For a comparison of holders of sovereign debt in various countries, see International Monetary Fund, World Economic and Financial Surveys: FISCAL MONITOR September 2011, Addressing Fiscal Challenges to Reduce Economic Risks (p. 12, Fig. 6). As can be seen from Figure 6 of the above IMF publication, while non-resident and foreign official holdings in the US (which still has a relatively healthy - though rapidly deteriorating - ratio of external to internal debt despite its recent past) are at 31%, for Japan, those holdings comprise a mere 5% of Government Debt.

16 Over the past twenty years mainland Chinese have, in increasing numbers (possibly in their millions, though no accurate figures are available), relocated and developed business enterprises in other regions of the world - chiefly in areas formerly recognized as 'developing' regions under Western control. While some commentators are now suggesting that this is part of some Chinese government plot to surreptitiously take over the 'developing' world, this needs to be put into historical perspective. Throughout the colonial period, Chinese traders followed in the wake of Western European colonial expansion. The 'Chinese trader' was an accepted part of the landscape of the colonial world, tolerated and regulated by colonial authorities. See Carl Trocki (2004) (Chinese capitalism and the British Empire. In International Association of Historians of Asia Conference, 6-10 December 2004, Taiwan, Taipei) for a description of this. As Trocki says, Because Chinese traders and migrants came without the support of their government, and in most cases were not seen to be organizing political domain over the region, they have not been portrayed as the frontiersmen of empire. There is likewise, little evidence that the Chinese involved, at least at the beginning, had the intention of forming an empire. Nevertheless, if we look at what had come to be in Southeast Asia at the end of the nineteenth century, it is clear that a Chinese empire of sorts had been created. ...Chinese relied on the European umbrella of security and found it possible to exploit the global reach of the European infrastructure. Europeans found they needed the Chinese to produce wealth for them and to manage the mundane tasks of retail and second-level wholesale trade. Neither could have prospered without the other but each was

guided by their own aims. Each was capable of taking measures to frustrate or

divert the projects of the other. We could say that Chinese and Europeans were

sleeping in the same bed, but were dreaming different dreams. It would be nice to believe that Chinese government authorities are willing (and able) to accept some sort of responsibility for the wellbeing of peoples around the world who currently find themselves at the exploited end of a resurgent Chinese small business expansion into the Third World. However, not only does the Chinese government accept little responsibility for the activities of these migrants, it has, to date, shown itself unable (possibly unwilling) significantly to protect Chinese migrants into its industrial regions as they find themselves in similarly exploitative working/living conditions. 17 A recent exchange with a friend (Japan/China historian, Lincoln Li) puts this into perspective: Just as the $ is used as a common denominator for the AU$, US$ etc., the three East Asian countries concerned have been using a common nomenclature. The Yuan, the Won, and the Yen are but different pronunciations for the same ideograph. All three countries have practiced parallel economic policies: feeding the insatiable consumer needs of the advanced countries (or should one say lazy and retarded countries) to "enrich the country and strengthen the military". And yes, they actually used the same medium of exchange in the days of silver. See China and Japan have agreed to start direct trading of their currencies for more on this. 18 See In Search of Utopia for more on this. |

Updated Version of The History and Nature of Capitalism - The Book

Why 'Third World' and why 'development'?

Articles/Books:

Capitalism, The Spirit of Christmas, a

bleak New Year and a hollow feeling in the pit of the stomach!

Capitalism, The Spirit of Christmas, a

bleak New Year and a hollow feeling in the pit of the stomach!

Capitalism, Renewable Energy, Ennui and the Fabled Ostrich: this

is as good as it gets!

Pre-empting Henry Hyde's Nightmare

Capitalism and Parables: It's all about gardening!

Global Capitalism: The Exploited Planet, the Torrent of Garbage

and The Warnings

The History and Nature of Capitalism - The Book

- Book Chapters:

- Introduction

- Ideology, The World Economic System and Revitalization Movements

- An Explanation and History of the Emergence of Capitalism

- How Born Again Christians Rescued Capitalism

- The Virtuous Capitalist, The Poor and the Wasteland

- Capitalism and Work: the White Man's Burden

- Capitalism and its Colonies

- Global economic forces, Western realities

- Global Capitalism, Third World Development

- Epilogue - What Drives Western People to Commoditize their World?

- Addendum: We're All Equal! Independence and Exchange

Links: